Paris, France – Fintep is pleased to announce its strategic partnership with Aether Financial Services. Fintep’s advanced Artificial Intelligence technology, Lucia, will now be available to Aether Financial Services’ suite of tools. The partnership will bring together Fintep’s highly flexible AI product with Aether Financial Services’ comprehensive financial services expertise in transaction management and agency services.

Captura de pantalla 2020-11-25 a las 11.28.52.png31.2 KB

The partnership with Fintep will allow Aether Financial Services to assist clients with a product powered by advanced machine learning technology across a multitude of use cases to optimize the management of their agencies and streamline their operations. This will enable Aether Financial Services to help clients process, extract, and analyze textual qualitative data faster, and deliver a seamless transaction/portfolio management solution and workflow that improves efficiencies and delivers value throughout the value chain.

Edouard Narboux, Founding Partner at Aether Financial Services said:

“We are delighted to announce this new strategic partnership with Fintep. We believe AI technologies are at the forefront of digital transformation in capital markets, and we want to be a part of that transformation. It is at the core of our DNA to provide the best service to our clients and by combining the know-how and expertise of our agency teams with Fintep’s cutting-edge AI technology, we will be able to deliver an unparalleled value proposition to our clients.”

Antonio Garcia, Chief Executive Officer of Fintep added:

“We have worked closely with Aether Financial Services to bring our best-in-class AI and agency technology to its diverse list of clients. Aether Financial Services’ expertise is a fantastic complement to our product’s unique capabilities, and we believe this partnership will bring real benefits to our end users. Together, it is a compelling proposition, and we are looking forward to working with Aether Financial Services to bring it to market.”

Andres Torrenti, Managing Director at Aether Financial Services added also:

“For Aether Financial Services, this partnership is a perfect fit. Fintep’s unique AI-powered platform integrates and extracts beautifully different data sources, and truly unlocks the power to use data to drive enterprise value, increase efficiencies across the value chain, and reduce exposure to operational risk through digitalization.”

About Aether Financial Services:

Aether Financial Services is a leader in post-transactional services, assisting issuers and investors, financial advisors, and lawyers in the valuation, closing management, and administration of debt and M&A documentation. Founded in 2015 to address the growing need for highly specialized agents in international loan and capital markets, Aether Financial Services is a leading independent transaction manager across different asset classes and jurisdictions. To learn more, visit us at www.aetherfs.com, and follow us on LinkedIn.

About Fintep:

Founded in 2017, Fintep plunges into this industry to build and deploy an innovative, next-generation technology software and cloud ecosystem. Our SaaS business model means that we can serve customers effectively, regardless of their size or location; from global financial institutions to community banks and credit unions. Fintep brings deep expertise and an unrivaled range of pre-integrated solutions from transaction banking to lending, and capital markets. With a global footprint and the broadest set of financial software solutions available on the market, Fintep manages more than 5 Trillion USD loans over 32 different jurisdictions including the top 100 banks globally. Visit us at https://fintep.com/ and follow us on LinkedIn.

For the past few years, the banking industry has been exploring the benefits of incorporating machine learning and artificial intelligence into their industry. In this regard, there have been significant advances in security, customer behavior recognition, sentiment analysis, trading recommendation systems, etc…

But after a few years, the industry has seen that the data that they have can only take them so far. Challenges like data quality, data tagging, pattern correlation vs causation, etc.… hit a wall when you only have so much data. When training an AI, engineers need more or different data that the banking entity currently has. And accessing external data sources often proves an impossible task due to security or privacy issues.

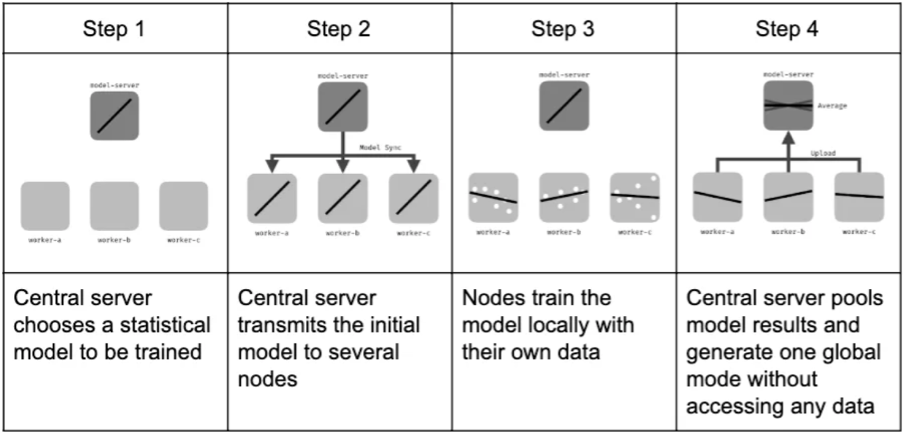

It is due to this necessity that federated learning has come into the light, since it permits different players to cooperate and share training data without compromising the privacy or security of their datasets. Not only that, but the extracted intelligence can be used for more than one industry player, encouraging cooperation between competitors in certain fields or different type of industries when their interests meet.

Federated learning also provides systems to adequately reward those players that contribute with higher or better quality data to the model training and to reject the entities whose data is of no value to the model that is being trained.

Imagen 1.png124 KB

If configured to do so, in the above image the model-server, implemented by a neutral entity, is capable of addressing the quality and quantity of the data that each player is bringing into the equation, and reducing the impact or, in extreme cases, flat out rejecting the data of one of the federated entities. Either by creating a new model from scratch or by re-training a model to include a new banking industry's intelligence, this approach ensures that the prediction quality will always be rewarding those who contribute the most.

Both in supervised and unsupervised approaches, it is clear that this technique can have a great value for future endeavors in machine learning. It will be through cooperation and not competition that the most powerful and advanced AI will be created in the future, simply because this approach will ensure access to the most varied and higher quality data, and in Fintep we are embracing this change with enthusiasm. As an African proverb says: “if you want to go fast, go alone. If you want to go far, go together”

Some banks are experimenting with rapid-automation approaches and achieving promising results. These trials have proved that automating end-to-end processes, which used to take 12 to 18 months or more, is doable in 6 months, and with half the investment typically required.

bank3-1.jpg122 KB

A European bank recently decided to automate its account-switching process. First, a team of IT, operations, and business-process experts analyzed existing processes from the customer, efficiency, and risk perspectives. The analysis uncovered several issues: more than 70 percent of the applications were paper-based, and of those, 30 to 40 percent contained errors and required reworking; applications often got stuck in one data-verification step for more than five days before being processed, and because of a lack of any IT integration, branch and back-office staff had to enter data manually from several systems into the workflow.

The team then defined what it wanted the process to look like, giving priority to operational and business impact (for instance, how much labor could be saved through automation) and to feasibility (such as how many new interfaces or changes to legacy systems would be required). The team focused on simplifying the process steps and procedural requirements at each stage—streamlining the information required from the customer and eliminating redundant verification steps—to reduce the complexity of the IT solution.

Using this design, the team carefully evaluated the possible integration options. It decided to use a combination of business-process-management software and Fintep’s AI extraction tool, in addition to the legacy systems, to create an automated and digitized workflow that did not significantly change existing IT systems. Daily huddles and weekly builds,2 which were immediately tested by users, ensured that the solution met the requirements, and kept users engaged.

As a result, the amount of time back-office staff spent handling account changeovers fell by 70 percent; the time customers needed to adjust to the switch was reduced by more than 25 percent. The cost-benefit ratio for this project was also significantly better than it had been in previous automation efforts: the project generated a return on investment of 75 percent and payback in just 15 months.

This European bank’s experience illustrates three principles that make success more likely when automating operations:

Consider business priorities to simplify the process. Automating inefficiencies or unnecessary product features embedded in historical processes is pointless. By first defining the best processes from the customer, business, and risk perspectives—taking a lean approach to process design—banks can significantly reduce what actually needs to be automated, which in turn lessens the cost, risk, and implementation time. A truly cross-functional team consisting of operations, IT, and business experts, as well as strong project governance, is required to design and enforce such optimal end-to-end solutions. The involvement of top management across multiple functions—operations, retail, and IT, for instance—is also essential.

Use multiple integration technologies and approaches. The right mix of integration solutions, backed by a solid evaluation of each solution’s time to market and contribution to architectural complexity, enables banks to automate most of their manual interventions without rewriting or substituting legacy architectural building blocks. For example, banks are successfully creating workflow systems by overlaying business-process-management tools that connect separate legacy systems, which in turn eliminates manual data entry and related errors across end-to-end processes. This evaluation is not straightforward, however, and requires a thorough understanding of what the market for integration solutions has to offer.

Prepare the IT shop for agile-development methods. To achieve rapid development cycles and use off-the-shelf solutions successfully, IT departments must build skills beyond their traditional capabilities. In particular, they should assess the software market and apply the right solutions; and capable of working seamlessly with business and operations counterparts.

As some banks experiment with this rapid-automation approach, and the impact of initial pilots resounds throughout the organization, IT and operations teams will feel pressured to integrate all end-to-end and back-office processes. All too often, however, efforts to scale up these initiatives are short-lived. IT architecture teams, concerned that they will not master unfamiliar integration solutions, or that additional efforts will make the IT landscape even more complex, may react warily. Meanwhile, operations and business personnel push to automate everything everywhere as soon as possible, without proper planning and evaluation. These pressures spread IT teams too thin, diverting their attention from the largest areas of opportunity. Because such projects are carried out much more quickly than traditional development efforts, IT departments struggle to set up the necessary infrastructure on time, and the teams are not focused on the value or necessity of additional features.

To overcome these obstacles, banks must design and orchestrate automation-transformation programs that prioritize and sequence initiatives for maximum impact on business and operations. They also need to define a target IT architecture (both applications and infrastructure) that uses a variety of integration solutions while maintaining a system’s integrity.

Successful large-scale automation programs need much more than a few successful pilots. They require a deep understanding of where value originates when processes are IT enabled; careful design of the high-level target operating model and IT architecture; and a concrete plan of attack, supported by a business case for investment.

Another European bank launched a strategic initiative to shrink its cost base and increase competitiveness through superior customer service. Upon completion of the first successful pilots, the bank’s automation program consisted of three phases.

In phase one, the bank examined ten macro end-to-end business processes, including retail-account opening and wholesale customer service requests, to identify the automation potential and to prioritize efforts.

In phase two, the architecture was designed and a plan of attack formulated. The bank took three critical actions:

It decided which processes would be fully automated, partially automated, or fully manual, based on four key tests. The tests determined whether a process was too complex to automate (for example, deal origination and structuring), whether regulation required human intervention (for instance, the financial-review process), whether or not the process was self-contained (that is, dependent on multiple customer or third-party interactions), and whether manual touchpoints added value to the customer relationship (for example, product inquiries).

It designed the building blocks of the target application architecture, which consisted of legacy systems and off-the-shelf applications such as Fintep Software, as well as the IT infrastructure requirements, to provide timely and necessary computing and storage.

It derived a design-based holistic business case for the automation program and defined the rollout plan.

In phase three, the bank implemented the new processes in three- to six-month waves, which included a detailed diagnostic and solution design for each process, as well as the rollout of the new automated solution.

This approach helped the bank to deliver business and operational benefits rapidly and successfully. The program paid for itself by the second year and kept implementation risks under control.

The dream of achieving rapid, large-scale process automation is becoming a reality for some banks. Competitors cannot afford to miss the opportunity to transform their own back-office processes.

shutterstock_1062744086-1.jpg136 KB

Banks have enhanced many of their customer-facing, front-end operations with digital solutions. Online banking, for example, offers consumers enormous convenience, and the rise of mobile payments is slowly eliminating the need for cash. But too many processes at banks still rely on people and paper. Often, back offices have thousands of people processing customer requests.

This high degree of manual processing is costly and slow, and it can lead to inconsistent results and a high error rate. IT offers solutions that can rescue these back-office procedures from needless expense and errors.

There is a significant opportunity exists to increase the levels of automation in back offices. By reworking their IT architecture, banks can have much smaller operational units run value-adding tasks, including complex processes, such as deal origination, and activities that require human intervention, such as financial reviews.

IT-enabling operations encompasses both automating processes (preventing customers from using paper, digitizing work flows, and automating or supporting decision making) and using IT solutions to manage residual operations that must be carried out manually (for example, using software for resource planning). By taking full advantage of this approach, banks can often generate an improvement of more than 50 percent in productivity and customer service!!!

Thanks to Fintep, some banks are already taking steps toward harnessing the considerable potential of this opportunity. For example, one of our existing customers, a large universal bank categorized its 900-plus end-to-end processes into three ideal states: fully automated, partially automated, and “lean” manual. This bank determined that 85 percent of its operations could—theoretically—be at least partially automated. At the time of this analysis, fewer than 50 percent of these processes were automated at all.

This scenario sounds promising and Fintep is happy to help you to achieve this task!!!

The concept of federated learning was first proposed by Google in 2017. Google’s main idea is to build machine-learning models based on datasets that are distributed across multiple devices while preventing data leakage and visibility. This type of machine learning does not lack of its own problems, such as communication cost in massive distribution, unbalanced data distribution, and device reliability. These factors must be taken into consideration when deciding whether to dive into this type of technologies, if only for the optimization difficulties. In addition, data is partitioned by user, entities or device Ids, therefore, horizontally in the data space.

But when it comes to data privacy-preserving machine learning approximations in a decentralized collaborative-learning setting, the advantages start to overcome the difficulties. Depending on the parties and data distribution involved, the privacy necessities or even the encryption adopted, multiple architectural approaches have been developed (Differential Privacy, Secure Multiparty Computation, Homomorphic Encryption, ...). But overall, there are two main architectural implementations of federated machine learning.

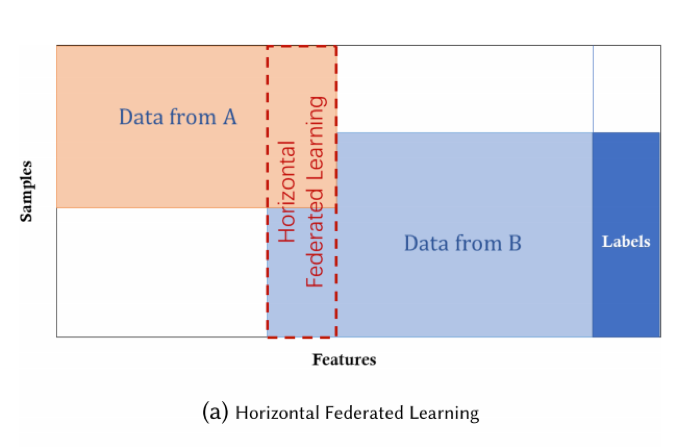

1. Horizontal Federated Learning

Horizontal federated learning, or sample-based federated learning, is introduced in the scenarios in which datasets share the same feature space but different space in samples.

Imagen 1.png43.5 KB For example, two regional banks may have very different user groups from their respective regions, and the intersection set of their users is very small. However, their business is very similar, so the feature spaces are the same. A collaboratively deep-learning scheme in which participants train independently and share only subsets of updates of parameters could make sense in this situation.

2. Vertical Federated Learning

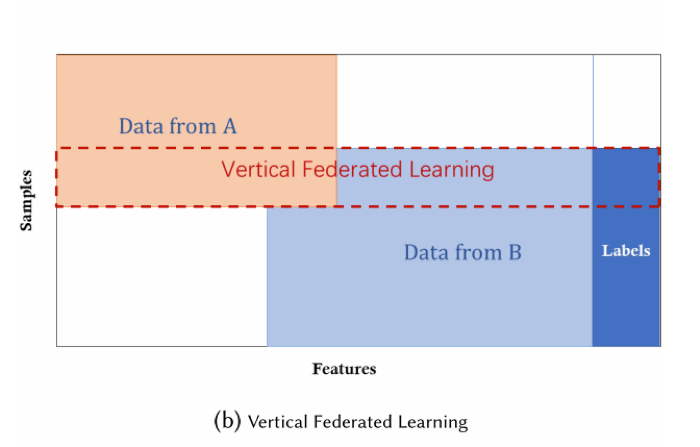

Privacy-preserving machine-learning algorithms have been proposed for vertically partitioned data, including cooperative statistical analysis, association rule mining, secure linear regression, classification, and gradient descent.

Imagen 2.png44.9 KB For instance, a vertical federated-learning approach would be fitting to train a privacy-preserving logistic regression model. The effect of entity resolution on learning performance and applied Taylor approximation to the loss and gradient functions so that homomorphic encryption can be adopted for privacy-preserving computations. Vertical federated learning or feature-based federated learning is applicable to the cases in which two datasets share the same sample ID space but differ in feature space.

For example, consider two different companies in the same city: one is a bank and the other is an ecommerce company. Their user sets are likely to contain most of the residents of the area; thus, the intersection of their user space is large. However, since the bank records the user’s revenue and expenditure behavior and credit rating and the e-commerce retains the user’s browsing and purchasing history, their feature spaces are very different. Suppose that we want both parties to have a prediction model for product purchases based on user and product information.

When diving into the world of machine learning, one of the most challenging tasks for an AI company is getting access to large amounts of relevant data, specially in a world as sensitive and private as the banking industry. Banks have long ago understood the value of their data, but they struggle when considering the best way of monetizing it while preserving user´s confidential data. Furthermore, the quality of any machine learning model and AI is limited by the amount and type of data that is trained with, which limits the quality of the predictive models to only the data that each of the entities holds within its systems.

This is why in Fintep, we have adopted a new way of training, maintaining and improving upon our AI: Federated Machine Learning. This approach allows each of the participants in the federated system to contribute and benefit from the training of an AI with the data never leaving their own datacenters, and also minimizing the number of transactions with the outside world, thus reducing possible security threats.

Another advantage that this technique brings into the table is the training speed and market adaptability. Let´s take for instance a problem that a lot of our clients are struggling with right now: LIBOR transition. Given the fact that this has been a relatively recent need in the banking sector, there was no model to deal with this eventuality. Traditional machine learning systems would have required dataset preparation, model training and validation by each of the users separately, which would have resulted in a costly, lengthy task, and with low to medium accuracy depending on the dataset size of each of the entities. But with Federated machine learning, most of this work can be shared without compromising the data, thus extremely accelerating the time to market of functional models as well as increasing significantly the accuracy of the extraction engine.

In this unprecedented time, corporate borrowers are concerned about access to liquidity as well as compliance with payment and other obligations under their credit documents.

We have recently seen various government regulators focused on ensuring that financial institutions work with issuers. For example, the Executive Order 202.9, issued by New York State Governor Andrew M. Cuomo on Saturday, March 21, 2020, declares it an “unsafe and unsound business practice” if a bank does not grant forbearance to a business that has a financial hardship as a result of the COVID-19 pandemic. The Interagency Statement on Loan Modifications and Reporting for Financial Institutions Working with Customers Affected by the Coronavirus, issued by the board of governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, the Office of the Comptroller of the Currency, the Consumer Financial Protection Bureau and the State Banking Regulators encourages financial institutions to “work prudently with borrowers who are or may be unable to meet their contractual payment obligations because of the effects of COVID-19.”

While these statements and orders may not be binding, they are instructive as to the current environment in which we expect lenders will appreciate the financial peril facing their borrowers and the need to work together to formulate creative and collaborative solutions to ensure their financing arrangements do not present an impediment to recovery.

Here are some good examples of borrower-friendly amendments that could be managed by Fintep’s integrated amendment management tool that will help borrowers to stay afloat until the economy gets up and running again:

1.Preserving Liquidity

a. Defer interest payments or interest being paid-in-kind, in each case, until a specified date.

b. Defer principal amortization payments or principal being paid-in-kind, in each case, until a specified date.

c. Consider deferring 2020 administrative agency and collateral agency fees and other fees on a deal-by-deal basis.

d. Waive or defer 2019 and 2020 Excess Cash Flow mandatory pre-payments.

e. Consider waiving or deferring other mandatory pre-payments on a deal-by-deal basis.

f. Consider modifications to the disposition of assets provisions to permit, as applicable, (a) licensing intellectual property, (b) selling unused or obsolete inventory, (c) factoring receivables or other assets, and (d) accelerating settlements related to third-party claims.

g. Remove some restrictions around equity cures, such as allowing cures during the fiscal quarter and allowing for cures beyond the amount necessary to comply with financial covenants.

h. Exclude the impact of COVID-19 from the Material Adverse Effect definition so it is no longer a concern when bringing down representations in borrowing notices.

i. Consider building in the ability to participate in applicable government bailout programs such as SBA loans.

2.Financial Covenant Compliance

a. Reset financial covenant holidays or financial covenant levels, in each case, until a specified date.

b. Addition of EBITDA add-back for fees, costs, losses, charges, expenses and lost profits and revenues in connection with any natural disaster, pandemic, epidemic, disease outbreak, or other public health emergencies (including the Coronavirus Disease 2019 (COVID-19) or any similar or related disease caused by the SARS-CoV-2 virus), including any such items related to sourcing new supply chains.

c. Consider modifications to relevant Consolidated Net Income adjustments and/or EBITDA add-backs, as applicable: (a) extraordinary, unusual, one-time or non-recurring fees, costs, losses, charges and expenses, (b) fees, costs, losses, charges and expenses relating to facility or operational shutdowns, (c) business interruption and other insurance proceeds, (d) reimbursable or indemnifiable costs, losses, charges, and expenses, (e) restructuring fees, costs, losses, charges, and expenses, (f) cost-savings initiatives, (g) goodwill impairment and (h) lost profits and revenues.

3.Financial Reporting Requirements

a. Extend the deadline for delivery of 2019 and 2020 audited financial statements (and related compliance certificates on a deal-by-deal basis) and, if necessary, revise credit agreement to permit a going concern qualification relating to COVID-19 effects.

b. Extend deadline for delivery of 2020 quarterly and/or monthly unaudited financial statements (and related compliance certificates on a deal-by-deal basis).

4.Events of Default

a. Waive default interest or convert default interest to be paid-in-kind.

b. Waive the cross-defaults to certain indebtedness, if applicable, or material agreements.

c. Review all Events of Default to determine whether any other default waivers are needed.

5.Eligible Assignees; Loan Assignments and Participations

a. Prevent lenders from assigning or participating the loans (including to a “Disqualified Institution”) without the borrower’s prior written consent.

b. If not already included, amend credit agreement to provide the ability for private equity sponsors to purchase the loans subject to customary caps and voting limitations.

6.ABL Facility Considerations

a. Reduce excess availability or liquidity triggers due to greater-than-expected cash outlays due to COVID-19 expenditures.

Fintep has several ways of elevating the agency position by improving the workflow. Functions like Document sharing, digital waiver and amendment management, and customized live deal pages with the agent, lender, and borrower views. The tool we offer handles communication exchange between agents and participants more efficiently.

If you are interested in all we offer to improve the workflow within the syndicated loan processes, you can find more information in the website or contact us!

With the ongoing uncertainty surrounding the economic effects of corporate responses to the pandemic, the most pressing issue for many borrowers in the short term is the preservation of liquidity, and the ability to access additional liquidity, in the face of falling revenues.

0.jpeg60.7 KB

Borrowers may look to proactively manage operations to ensure that no mandatory prepayment is required under their loan agreement because an excess cash flow sweep is triggered. Many loan agreements now afford borrowers considerable flexibility to reduce excess cash flow sweeps, often on a dollar-for-dollar basis.

Many recent loan agreements afford borrowers considerable flexibility to raise incremental short-term senior debt or to segregate assets to secure financing provided by liquidity providers through, for example, an unrestricted subsidiary.

Finally, depressed debt trading prices may present a deleveraging opportunity for borrowers who can cancel the debt at less than par and reduce the interest burden.

A close analysis of the loan agreement is required, and we are here in Fintep to help you!

Should a breach of a financial covenant occur, an equity cure right is a right for the shareholders to invest additional equity or subordinated debt into the Group to cure that breach.

bigstock-165491822.jpg225 KB

The standards applicable to equity cures have been loosened in favor of borrowers in recent years. Traditionally, borrowers have had the opportunity to cure a ratio breach, with the cure amount used to notionally reduce total net debt. A stronger position increasingly obtained by borrowers is for the cure amount to be added to EBITDA, flattering to the relevant ratio.

Fintep will help you to answer the following points: · Timing deadlines for an equity cure being implemented. · How the cure amount is to be applied? · Whether there is a requirement to repay debt using any portion of the equity cure amount and whether there is a restriction on “over cures”? · How the equity cure amount is treated for future financial covenant tests once injected; is the relevant cash required to be retained by the business? · Restrictions on equity cure rights in terms of quantum and number per financial year or in consecutive testing periods?

Fintep’s Federated Machine Learning technology stack to improve your accuracy levels in your Artificial Intelligence Banking applications. Fintep Loan platform, Lucia, will provide your institution the scale of a larger training data set, while maintaining your data privacy and security on your premises or private cloud. Read Antonio García Romero’s article to learn more.

When processing syndicated loans, it is often the case that relevant information can only be found in in-text references that, more often than not, reference data in other documents.

It is for this very reason that Fintep has invested time and efforts developing cutting edge technology to be able to properly follow a trace of references across a multi-type legal document environment. Working with open source technologies and in-house build training datasets, we have successfully specialised our probabilistic models to work with legal language, obtaining a high degree of accuracy in nested data.

AI and automation disruption are gaining ground in the syndication arena, and with this technology Fintep will get a solid differentiate value added to our clients.

Although “covenant-lite” credit facilities have become more common in the U.S. and Europe in recent years, a material drop in a borrower’s earnings will have an adverse impact on its cash flows and may drive companies to become more reliant on their revolving facilities for future liquidity needs. This increased usage by borrowers of their revolving facilities could trigger related springing maintenance test thresholds in loan financing documents.

0.jpg23.6 KB

Lenders will need to scrutinize certain financial covenant related definitions (such as “consolidated net income” and “consolidated EBITDA” and similar terms) in loan documents carefully to determine if add-backs (such as for cost savings, synergies or other permitted initiatives) could be utilized to limit the amount of covenant impact resulting from decreased net income or EBITDA. Adjustments to the definition of “consolidated EBITDA” may have implications beyond financial covenant compliance such as step-downs for the asset sale and excess cash flow mandatory prepayment provisions, certain covenant baskets (such as additional debt and lien incurrences) and possibly pricing step-downs.

When processing syndicated loans, it is often the case that relevant information can only be found in in-text references that, more often than not, reference data in other documents.

It is for this very reason that Fintep has invested time and efforts developing cutting edge technology to be able to properly follow a trace of references across a multi-type legal document environment. Working with open source technologies and in-house build training datasets, we have successfully specialised our probabilistic models to work with legal language, obtaining a high degree of accuracy in nested data.

AI and automation disruption are gaining ground in the syndication arena, and with this technology Fintep will get a solid differentiate value added to our clients.

Glad to announce Fintep has been selected as the top 6 Finalist by ABANCA and Lanzadera Corporate Fintech Program. This program has the goal to select most innovative startups in capital markets, payments, customer engagement, neobanks, enterprise solutions and wealth management.

Non-performing loans: Council adopts position on secondary markets for bad loans

The EU is encouraging the development of secondary markets for non-performing loans (NPLs), which would allow banks more easily to manage or sell bad loans. EU Ambassadors have recently approved the Council's position on a proposed directive which harmonises rules for how non-credit institutions can buy credit agreements from banks. The aim of the new rules is to reduce existing banks’ stocks of NPLs and prevent their accumulation in the future.

image.png1.5 MB

Currently, potential buyers of bad loans face barriers to cross-border purchases of credit due to different regulatory regimes in the member states. This has led to an inefficient secondary market for NPLs, with low demand, weak competition and low bid prices. The proposed new directive removes obstacles to the transfer of NPLs from banks to non-credit institutions, and simplifies and harmonises the authorisation requirements for credit services across the EU, without prejudice to national rules imposing certain additional requirements on credit services.

Thanks to Fintep, banks can benefit of this new regulation and automatize this secondary trading selling process! More info, please contact us!

Wondering which part of your loan book is subject to Federal Reserve’s collateral program? As you may know, this program applies to financial institutions required to pledge acceptable securities as collateral to secure deposits of U.S. federal program agencies. Collateral pledged to Reserve Banks can be used to secure discount window advances and extensions of daylight credit or master account activity including charges associated therewith. 0.jpg13 KB As part of this process, each Financial Institution will have to take a look at the type of Security, duration, issuer, currency, positions… it’s a tiresome and time-consuming job that office bankers have to implement repeatedly looking at different sources of information.

Thanks to Fintep, in a matter of minutes, you could easily identify those loans that are pledgeable at the FED based on the terms of the loans as identified by Fintep’s Lucia Platform!!

Financial Institutions seek protection in new software tools: Software companies probably will emerge from the coronavirus downturn in even better shape than they were before the pandemic upended business activity across the world. With social distancing likely to remain a feature of life for the foreseeable future, demand for software is growing robustly.

0.jpg24.2 KB

Indeed, according to Bank of America, more than half of top organizations intend to increase their software spending this year, at a time when overall investment is shrinking (banks are reducing cost but investing in software solutions). In a survey of 500 financial businesses, it concluded that “software budgets appear to be up post-Covid. Spend is strongest for modern, digital and cloud-based products for investment banking.” Banks are moving fast to be as well prepared as possible to reduce time of execution, manual risk and redundancies, improve internal efficiency and seeking for protection in new software tools. Tech platform Fintep provides advanced security layers from networking, user access and data encryption. More doubts? please contact us!

The liquidity that rapidly flooded the treasury and corporate bond markets has been slower to reach the syndicated loan market. However, the US Federal Reserve’s Main Street lending program is now live.

01.jpg58.3 KB

The delay in bringing the Main Street lending facility stems from the complexity and unstructured nature of the loan market. The bucket that will be utilized for syndicated loans will be the Main Street Expanded Lending Facility (“MSELF”). MSELF allows a borrower to upsize an existing eligible loan in an amount from $10 million to $300 million. Navigating eligibility and ensuring compliance with the existing documentation will present challenges. Furthermore, coordination among the lender group is required given the pari passu features of the MSELF loan. Tech platform Fintep streamlines communication between the agent, borrower, and lenders which could speed adoption of MSELF liquidity. More doubts? please contact us!

According to Bain&Company, improving contract management can yield 100 basis points of restored revenue, which drops right to the bottom line. Article reinforce the idea that many Financial Institutions are leaking large sums of cash due to sloppy contract management. Unfortunately too often, a contract goes into an electronic drawer where it cannot be easily accessed, analysed or tracked.

01.jpg33.4 KB

Wringing full value from contracts requires an airtight contract structure and robust fulfilment. Building mature capabilities entails steps that include a single data house with easy access, processes supported by the right digital tools, coaching for the front line and accountability for contract enforcement. Feel yourself in this situation? Please contact us! www.fintep.com/intro